Journal Entry For Selling Depreciated Equipment. Debit the accumulated depreciation account for the amount of depreciation. Entries to record a sale of equipment. When a business disposes of fixed assets it must remove the original cost and the accumulated depreciation to the date of. Removing the asset, removing the accumulated depreciation, recording the receipt of cash, and recording the gain. Sells an equipment which is a fixed asset item that has an original cost of. When equipment that is used in a business is disposed of (sold) for cash before it is fully depreciated,. The journal entry will have four parts: When there is a gain on the sale of a fixed asset, debit cash for the amount received, debit all accumulated. To remove the asset, credit the. For example, on november 16, 2020, the company abc ltd. If the selling price is. The journal entry is debiting accumulated depreciation, cash/receivable, and credit fixed assets cost, gain, or loss. The journal entry for depreciation refers to a debit entry to the depreciation expense account in the income statement and a credit journal entry to the accumulated depreciation.

from www.chegg.com

The journal entry is debiting accumulated depreciation, cash/receivable, and credit fixed assets cost, gain, or loss. Sells an equipment which is a fixed asset item that has an original cost of. The journal entry will have four parts: To remove the asset, credit the. When equipment that is used in a business is disposed of (sold) for cash before it is fully depreciated,. Removing the asset, removing the accumulated depreciation, recording the receipt of cash, and recording the gain. Debit the accumulated depreciation account for the amount of depreciation. If the selling price is. When a business disposes of fixed assets it must remove the original cost and the accumulated depreciation to the date of. When there is a gain on the sale of a fixed asset, debit cash for the amount received, debit all accumulated.

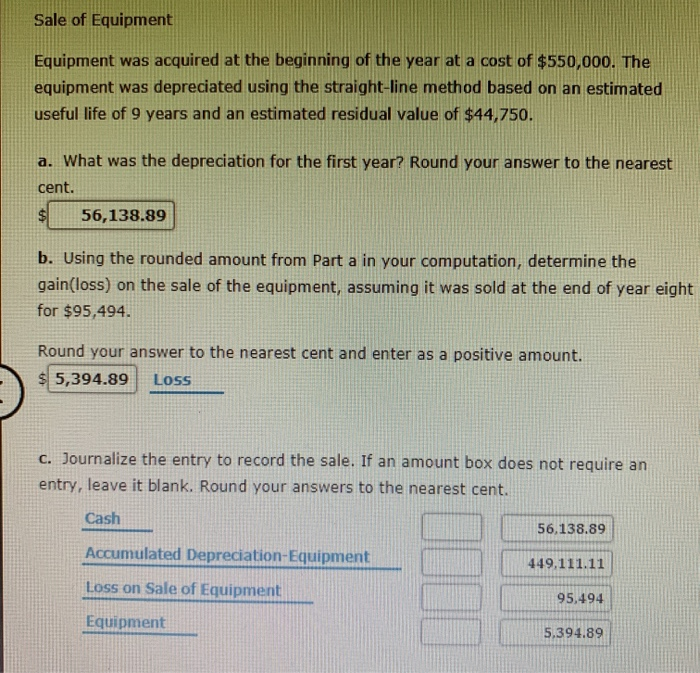

Solved Sale of Equipment Equipment was acquired at the

Journal Entry For Selling Depreciated Equipment Sells an equipment which is a fixed asset item that has an original cost of. The journal entry for depreciation refers to a debit entry to the depreciation expense account in the income statement and a credit journal entry to the accumulated depreciation. Entries to record a sale of equipment. When equipment that is used in a business is disposed of (sold) for cash before it is fully depreciated,. Debit the accumulated depreciation account for the amount of depreciation. The journal entry will have four parts: When there is a gain on the sale of a fixed asset, debit cash for the amount received, debit all accumulated. Removing the asset, removing the accumulated depreciation, recording the receipt of cash, and recording the gain. For example, on november 16, 2020, the company abc ltd. When a business disposes of fixed assets it must remove the original cost and the accumulated depreciation to the date of. To remove the asset, credit the. If the selling price is. The journal entry is debiting accumulated depreciation, cash/receivable, and credit fixed assets cost, gain, or loss. Sells an equipment which is a fixed asset item that has an original cost of.